News, Blogs and Notices

News, blogs and notices

Delve into the latest news, information and opinions.

Click on the tabs below to select news, blogs or notices.

Displaying 1 - 18 of 953

news

Minister O’Gorman Launches the Childminding Development Grants for 2024

news

Last Chance to Apply for Training Links – Deadline: Friday, 17 May

news

Minister Byrne Launches Participation Nation Outdoor Fund

news

Music Network Music Capital Scheme 2024 Inviting Applications

news

Training Links: A Training Network at Work

news

Public Hearing: How Can Taxation Systems Better Support the Social Economy?

news

New Report Published: “That's Not Your Role” State Funding and Advocacy in The Irish Community Voluntary and Nonprofit Sector

news

The Future Is Community - The Wheel's Local Election Campaign Pledge Launched

news

The Charities Regulator Wants Your Views on the Governance Code

news

Training Links - Explore Our FAQs for Answers!

news

Coca-Cola Thank You Fund 2024 Opens!

news

Training Links – Your Questions Answered

news

Practitioner Workshop on the Transformative Power of Community Education for Lone Parents, 9 May

news

Summit 2024 Programme Announced!

news

Apply for the Heart of the Community Fund 2024

news

We are Recruiting: Director of Development and Member Services

news

Read the Latest Edition of The Social Economy Insider

news

Our Rural Future: Minister Humphreys Announces €8.7 Million in Funding for Community and Sports Facilities

Displaying 1 - 18 of 152

blog

How Can Taxation Systems Better Support the Social Economy?

blog

Updates from Ivan

blog

The loneliest country in Europe must not take its community supports for granted

blog

The Wheel Wins the Overall Award in Global Action Plan’s National Climate Competition

blog

Season's Greetings and a Special Message from The Wheel's CEO

blog

#OurEUStory Award winners announced at 2023 Access Europe Showcase

blog

Guest Blog: The Mirror Never Lies - Unmasking the Illusion of Hybrid Working

blog

Ending Food Poverty: Making a Case for Casework

blog

Social Finance Foundation - Charting Growth in Latest Annual Report

blog

Exciting News: PayPal Giving Fund Ireland Announces Launch of Small Charities Campaign #OneTapBigImpact

blog

It’s Not So “Lonely at the Top” – When You have a Mentor!

blog

Three Priorities This Month To keep you in the loop about the work we do on your behalf, here’s a brief update about three priorities on The Wheel’s radar this month.

blog

Funding, Collaboration, Unity, Leadership, Sustainability, Integration: The Summit 2023 Parallel Sessions

blog

On National Workplace Wellbeing Day (28 April), Charity Workers Face Increasing Pressures and Inadequate Pay

blog

The Rise of Ransomware: Understanding the Threat and Protecting Your Nonprofits’ Data

blog

Enhancing the Governance of Charities

blog

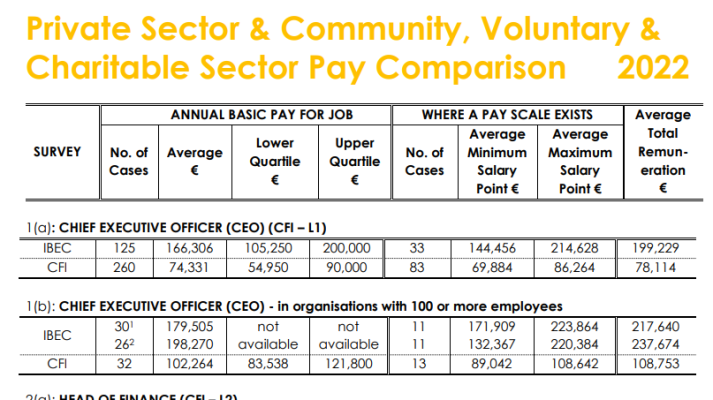

Private Sector Comparator Data Released for 2022 Pay & Benefits Report

blog

International Women’s Day 2023: Equity & Leadership

Highlight Your Events and Initiatives On the Community Noticeboard

Displaying 1 - 18 of 1762

notice

Open Call: Apply to join the Panel of Artists and Creative Facilitators for The National Neighbourhood

notice

Richmond Barracks Summer Fair, 25 & 26 May

notice

Open Call: Apply to join the Panel of Artists and Creative Facilitators for Richmond Barracks

notice

Limerick-based Charity, Cliona’s Foundation Named as Winner of Health and Wellbeing Draw

notice

FREE Suicide Bereavement Support Services Awareness Evening, 13 June

notice

Alone Conference 2024: Collaborating - Our Collective Responsibility

notice

Filing Cabinets for Donation

notice

HUGG Free Information Event - Finding Hope and Healing After Suicide, 15 June

notice

Why “other people” are to blame when conflict occurs and how not to BRAG (Blame, Revenge, Anger, Guilt) about it when it happens! Free Zoom Webinar, 17 May

notice

Interwoven Lives, Threads of Hope: Exclusive Interview with UNFPA’s Jacqueline Mahon

notice

IGHN Conference 2024 - Fostering Humanity: Promoting Health Equity for a Better Planet

notice

Webinar: Lunch & Learn - Experiencing Grief as a Volunteer

notice

Sensational Kids Announces Groundbreaking for New National Child Development Centre in Kildare Town

notice

HUGG Volunteer Information Session, 23 May

notice

Applications Now Open for the Ideas Collective

notice

TU Dublin Education Fair for Traveller and Roma Communities, 28 May

notice

Bridging Lives: The Impact of Media, Community, and Organ Donation A reflection on Organ Donor Awareness Week 2024

notice

€1,090,700 in funding announced for the Music Capital Scheme 2024, along with two new awards

Displaying 1 - 13 of 13

podcasts

The Problem of Parity - Season 4 Ep 1

podcasts

The Good Stuff: Year in Review 2021

podcasts

The Good Stuff (Special Episode): Trustee Week 2021

podcasts

The Good Stuff (Special Episode): Where Next for Nonprofits?

podcasts

Human Conversations — The Language of Empathy (Season 3, Episode 3)

podcasts

Say What You Mean — Plain English for Nonprofits (Season 3, Episode 2)

podcasts

Words Matter — The Language of Nonprofits (Season 3, Episode 1)

podcasts

Organisational Resilience During COVID-19 — HR and Fundraising for Nonprofits (Season 2, Episode 3)

podcasts

Resilience vs Resistance — Pursuing Policy Change During the COVID-19 Crisis (Season 2, Episode 2)

podcasts

Resilience in Theory and in Practice (Season 2, Episode 1)

podcasts

Episode 3 of The Wheel's New Podcast, The Good Stuff

podcasts

Episode 2 of The Wheel's New Podcast, The Good Stuff

podcasts

Episode 1 of The Wheel's New Podcast, The Good Stuff