News, Blogs and Notices

News, blogs and notices

Delve into the latest news, information and opinions.

Click on the tabs below to select news, blogs or notices.

Displaying 1 - 18 of 940

news

Summit 2024 Programme Announced!

news

Apply for the Heart of the Community Fund 2024

news

We are Recruiting: Director of Development and Member Services

news

Read the Latest Edition of The Social Economy Insider

news

Our Rural Future: Minister Humphreys Announces €8.7 Million in Funding for Community and Sports Facilities

news

Are You Interested in Applying for a Training Links Grant?

news

UC: Excellent Business Summer Interns Available for 6 weeks (Unpaid)

news

Applications Invited for Communities Integration Fund 2024

news

Application for Funding With Training Links - Is My Organisation Eligible?

news

National Lottery Good Causes Awards 2024 Now Inviting Applications Until 12 April

news

Summit 2024: Get Your Ticket Now!

news

Book Your Place for Accredited Social Return on Investment Training

news

Invest in Upskilling with a Training Links Grant

news

Dublin Learning City Festival 2024 - Applications Now Open to Host Events

news

Public Consultation on the Draft Regulations for Childminders - Have Your Say

news

Training Links 2024-2026 Applications Now Open

news

Call for Chairperson and Ordinary Members for Policing and Community Safety Authority

news

Summit 2024: Early Bird Offer Closing 29 March

Displaying 1 - 18 of 151

blog

Updates from Ivan

blog

The loneliest country in Europe must not take its community supports for granted

blog

The Wheel Wins the Overall Award in Global Action Plan’s National Climate Competition

blog

Season's Greetings and a Special Message from The Wheel's CEO

blog

#OurEUStory Award winners announced at 2023 Access Europe Showcase

blog

Guest Blog: The Mirror Never Lies - Unmasking the Illusion of Hybrid Working

blog

Ending Food Poverty: Making a Case for Casework

blog

Social Finance Foundation - Charting Growth in Latest Annual Report

blog

Exciting News: PayPal Giving Fund Ireland Announces Launch of Small Charities Campaign #OneTapBigImpact

blog

It’s Not So “Lonely at the Top” – When You have a Mentor!

blog

Three Priorities This Month To keep you in the loop about the work we do on your behalf, here’s a brief update about three priorities on The Wheel’s radar this month.

blog

Funding, Collaboration, Unity, Leadership, Sustainability, Integration: The Summit 2023 Parallel Sessions

blog

On National Workplace Wellbeing Day (28 April), Charity Workers Face Increasing Pressures and Inadequate Pay

blog

The Rise of Ransomware: Understanding the Threat and Protecting Your Nonprofits’ Data

blog

Enhancing the Governance of Charities

blog

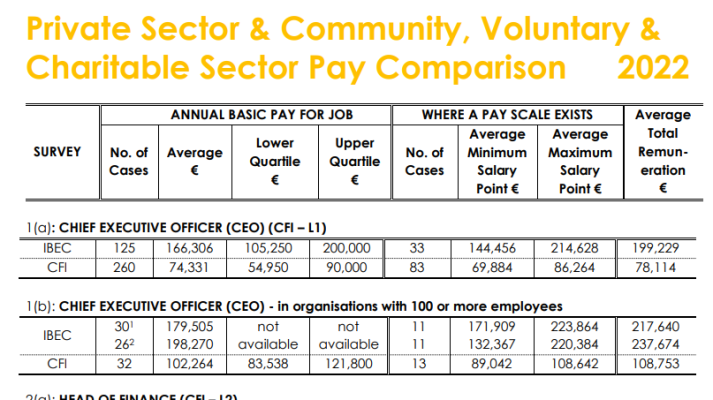

Private Sector Comparator Data Released for 2022 Pay & Benefits Report

blog

International Women’s Day 2023: Equity & Leadership

blog

Parting Words from Deirdre Garvey, Outgoing CEO of The Wheel

Highlight Your Events and Initiatives On the Community Noticeboard

Displaying 1 - 18 of 1731

notice

HUGG Volunteering Information Session, 18 Apr

notice

PILA Information Session & Survey for NGOs and civil society organisations

notice

Cloth Nappy Library Ireland announces Earth Baby Fair Line Up, 20 Apr

notice

Leadership Essentials in Global Health: Summer Programme - Trinity College Dublin, 19-24 Aug

notice

Call for Presentations - All-Island Social Security Network Conference, 20 June

notice

Friends of the Earth Ireland's 50th Anniversary Education Day, 27 Apr

notice

Online Report Launch: “That’s not your role”- State Funding and Advocacy in the Irish Community, Voluntary and Non-Profit Sector, 29 Apr

notice

Youth Advisory Panel

notice

Looking, Listening and Talking. How Doing Three Simple Things Differently and Better can Change Problems into Solutions and the past into the future! Free Zoom Webinar, 16 Apr

notice

Artists Play Hide and Seek as Incognito, Ireland’s Biggest Online Art Sale is Launched

notice

Upcoming Webinar for Employers: The Carer's Contribution

notice

Community Climate Action: Practitioners Training Programme

notice

Public Launch: Film showing, Poetry reading & Conversation, 7 May

notice

National Conference on Stroke, 20 May

notice

TU Dublin Report Launch & Seminars this May

notice

Sensational Kids Launches New E-Learning Programme to Support Children's Development

notice

Kildare’s Little Hill Animal Rescue & Sanctuary win Movement for Good Animal Special Draw in 2024

notice

Minister Humphreys launches 2024 SuperValu TidyTowns Competition

Displaying 1 - 13 of 13

podcasts

The Problem of Parity - Season 4 Ep 1

podcasts

The Good Stuff: Year in Review 2021

podcasts

The Good Stuff (Special Episode): Trustee Week 2021

podcasts

The Good Stuff (Special Episode): Where Next for Nonprofits?

podcasts

Human Conversations — The Language of Empathy (Season 3, Episode 3)

podcasts

Say What You Mean — Plain English for Nonprofits (Season 3, Episode 2)

podcasts

Words Matter — The Language of Nonprofits (Season 3, Episode 1)

podcasts

Organisational Resilience During COVID-19 — HR and Fundraising for Nonprofits (Season 2, Episode 3)

podcasts

Resilience vs Resistance — Pursuing Policy Change During the COVID-19 Crisis (Season 2, Episode 2)

podcasts

Resilience in Theory and in Practice (Season 2, Episode 1)

podcasts

Episode 3 of The Wheel's New Podcast, The Good Stuff

podcasts

Episode 2 of The Wheel's New Podcast, The Good Stuff

podcasts

Episode 1 of The Wheel's New Podcast, The Good Stuff